Only launched in 2022, Chinese-owned online retailer Temu has exploded on the scene to become one of the biggest online shopping platforms in the world today.

To better understand Temu’s meteoric rise, their current standing in the eCommerce industry, and where they might be headed in the future, we’ve put together a packet of statistics that tell you all you need to know about Temu, the company looking to disrupt the shopping app market.

Want weekly insights into how 7, 8 and 9-figure ecommerce brands are driving sustainable growth? That’s what you get with our value-packed newsletter, The Retention Edge. Subscribe for free today.

What is Temu?

Temu is an “everything” online shopping platform, selling virtually anything you can think of, from clothing to electronics to patio furniture.

The platform operates on a marketplace model, like Amazon, where many products are sold by individual third-party sellers. Where Temu sets itself apart is in price, advertising products at ridiculously low prices, such as an $8.99 smart watch, a tank top for $4.47 and a $9.39 dress.

Accompanying these products are advertisements for savings in excess of 90% off, limited-time deals, and a heavy focus on urgency and scarcity tactics.

While the press around Temu of late has been more negative than positive, you can’t argue against the platform’s success, currently sitting as the top shopping app in the US for both iPhone and Android, ahead of massive names like Amazon, Walmart and Shein.

Temu: Key Facts

Read more: in this article, we take a deep dive into the tactics used by brands like Temu and Shein to keep users hooked, and why mobile apps are at the core of it all.

Temu & Super Bowl 58

Many people were introduced to Temu by their high-profile Super Bowl advertisement in February 2024, which is estimated to have cost them $21 million in ad spend alone.

The company ran three 30-second ads during the most-watched television event since the moon landing. According to Business Insider, these ad spots cost $7 million each, putting their ad spend for 1:30 of airtime at a cool $21 million.

The $21 million Super Bowl ad spend is not all though; Temu ran three more ads after the game ended, and a company spokesperson stated that the ads were part of a wide campaign that featured “more than $15 million in coupons and giveaways.”

Key Temu Statistics in 2025

Now let’s explore some of the most notable Temu statistics you need to know today.

How Many People Use Temu?

Temu was only launched in September 2022. In less than a year, the platform already eclipsed 100 million active users in the US.

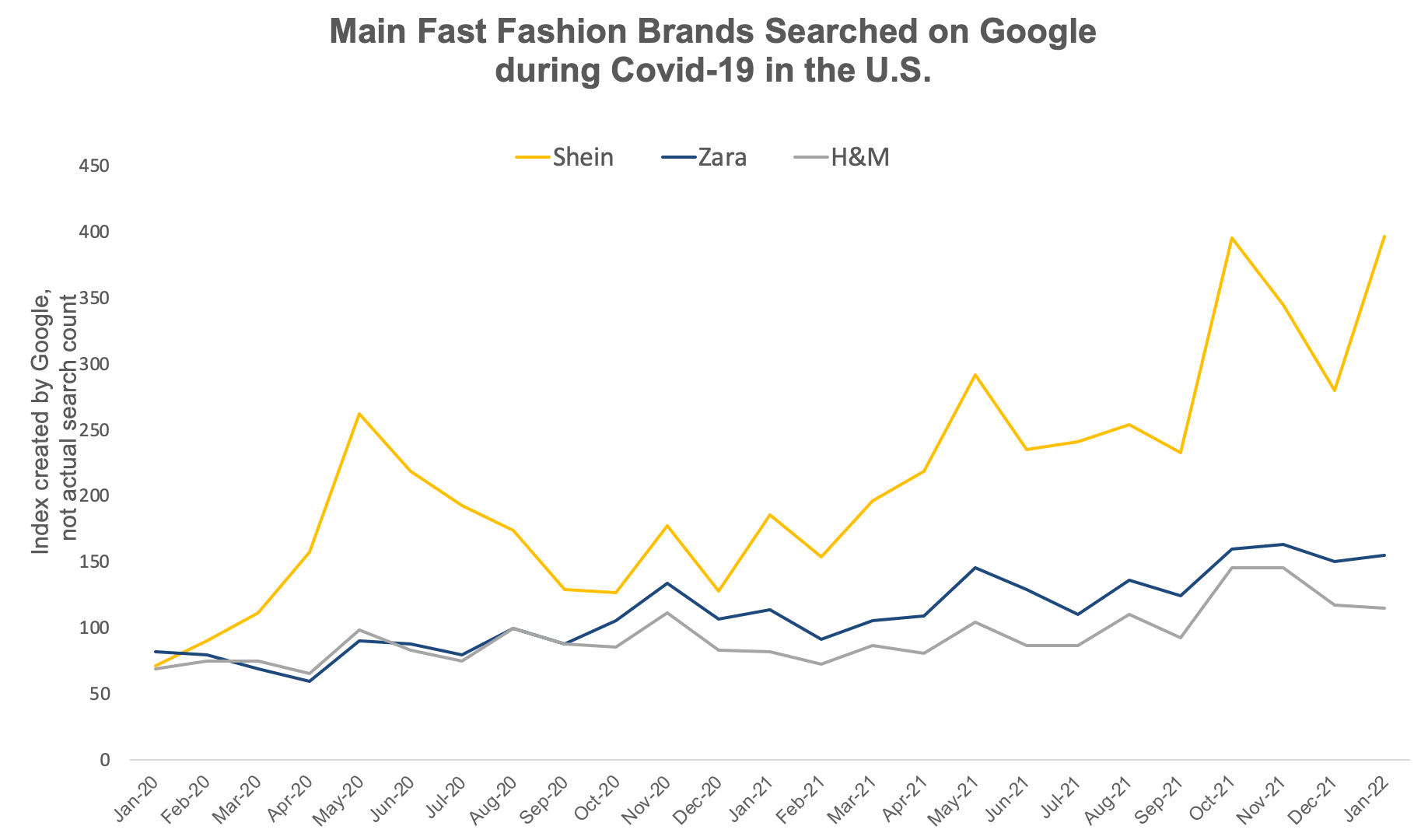

To put that in perspective, Shein has just 13.7 million users in the US (74.7 million worldwide – fewer than Temu’s user base in the US), while there are 112 million Amazon Prime users in the US.

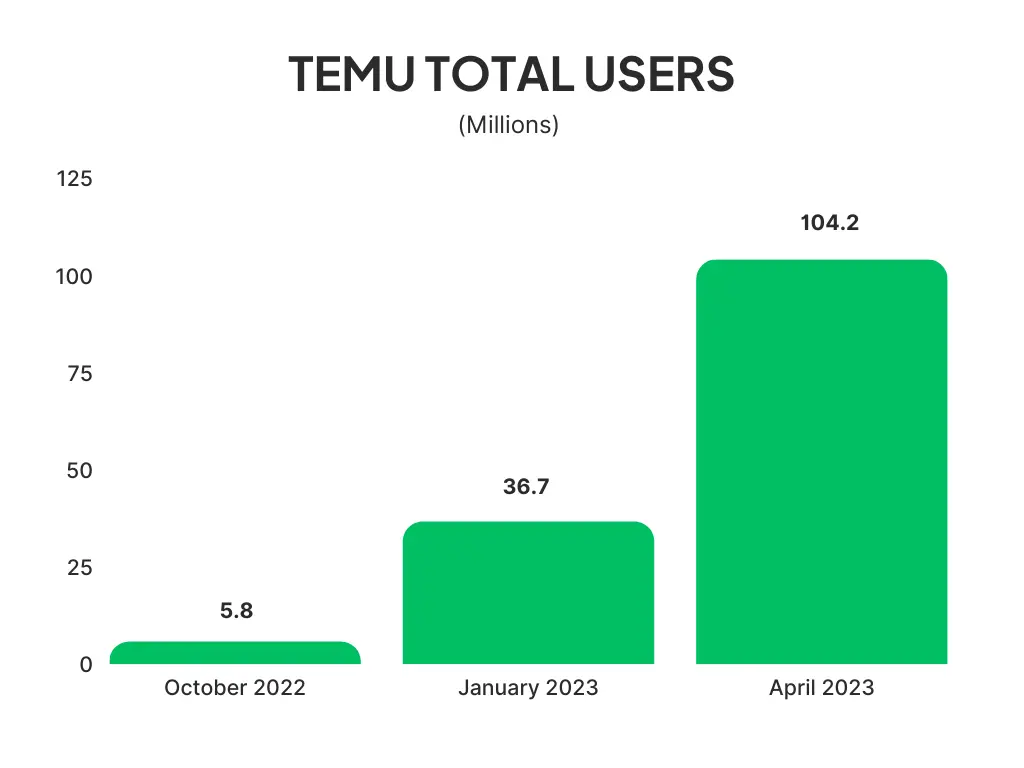

Temu Growth: 2022-23

Obviously, to go from zero to 100 million users in less than a year requires a steep growth curve. Temu’s growth is certainly no exception, going from 5.8 million US users in October 2022 to 104.2 million in April 2023.

Temu Revenue & Sales

Temu’s monthly GMV in September 2022 was estimated to be $3 million, jumping to $192 million for January 2023.

The platform’s revenue has since exploded further, reportedly doing $3 billion in revenue in the first half of 2023. With this figure, we can estimate Temu’s yearly revenue is at least $6 billion.

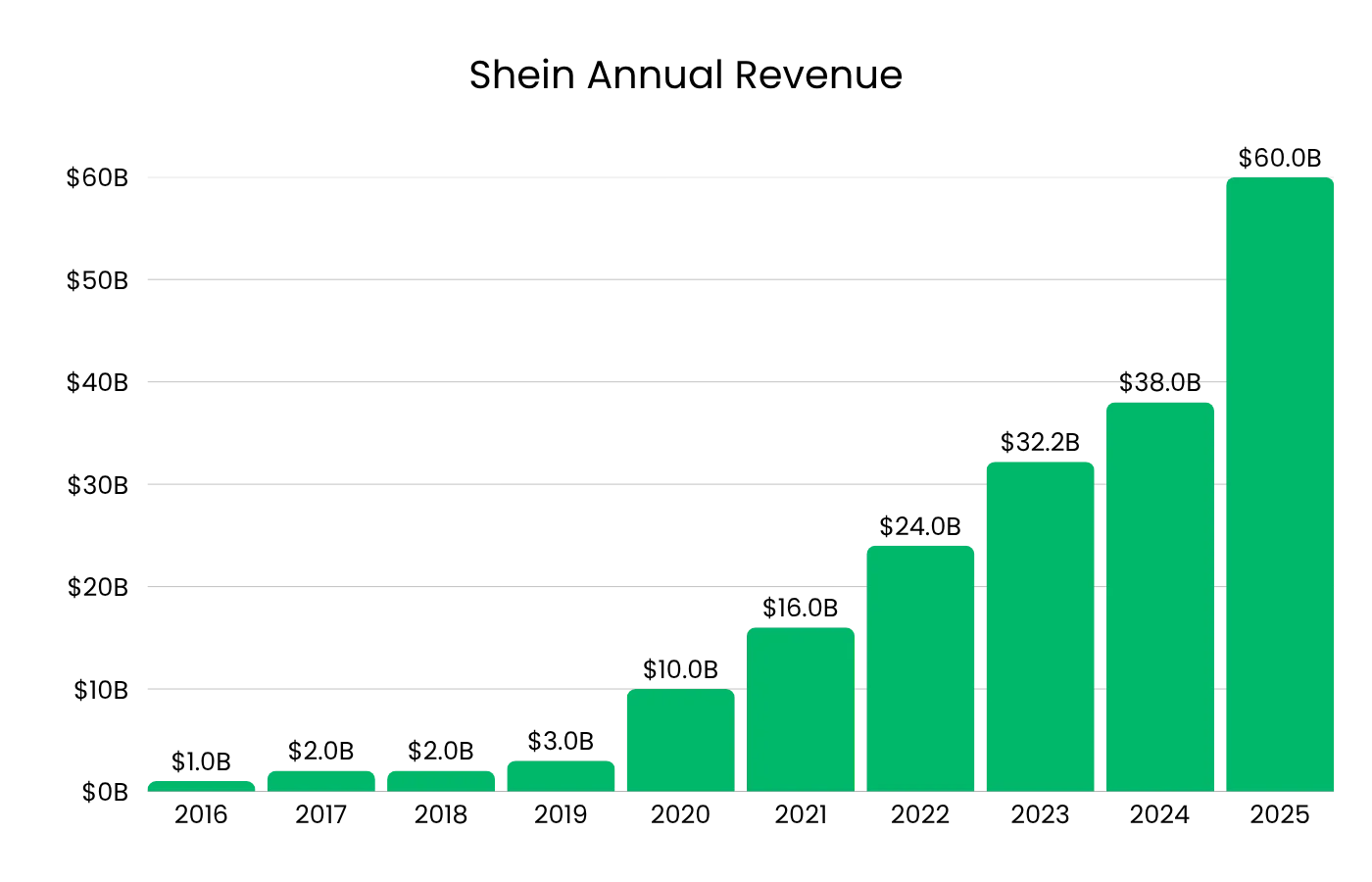

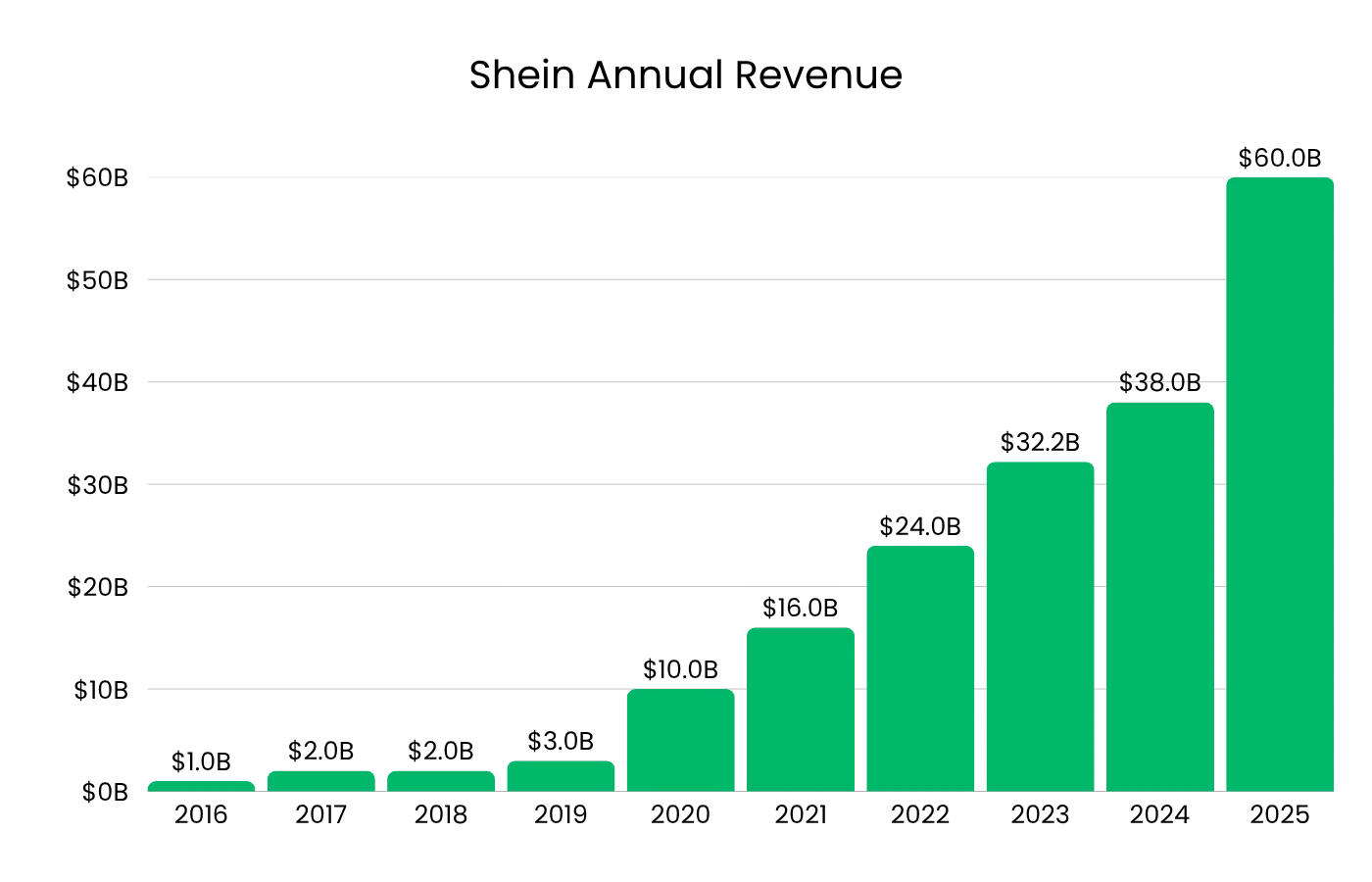

For reference, competitor Shein’s annual revenue is $24 billion. Temu’s lower revenue, despite having a higher user base, can be attributed to their focus on low-priced discount items leading to a much lower average spend per customer.

Both are still significantly behind Amazon, which generates nearly $700 billion globally in revenue per year, as the eCommerce leader in the American market.

For one more comparison, Temu’s sister company Pinduoduo (owned by the same parent company, PDD Holdings), did the equivalent of US$19 billion revenue in 2022.

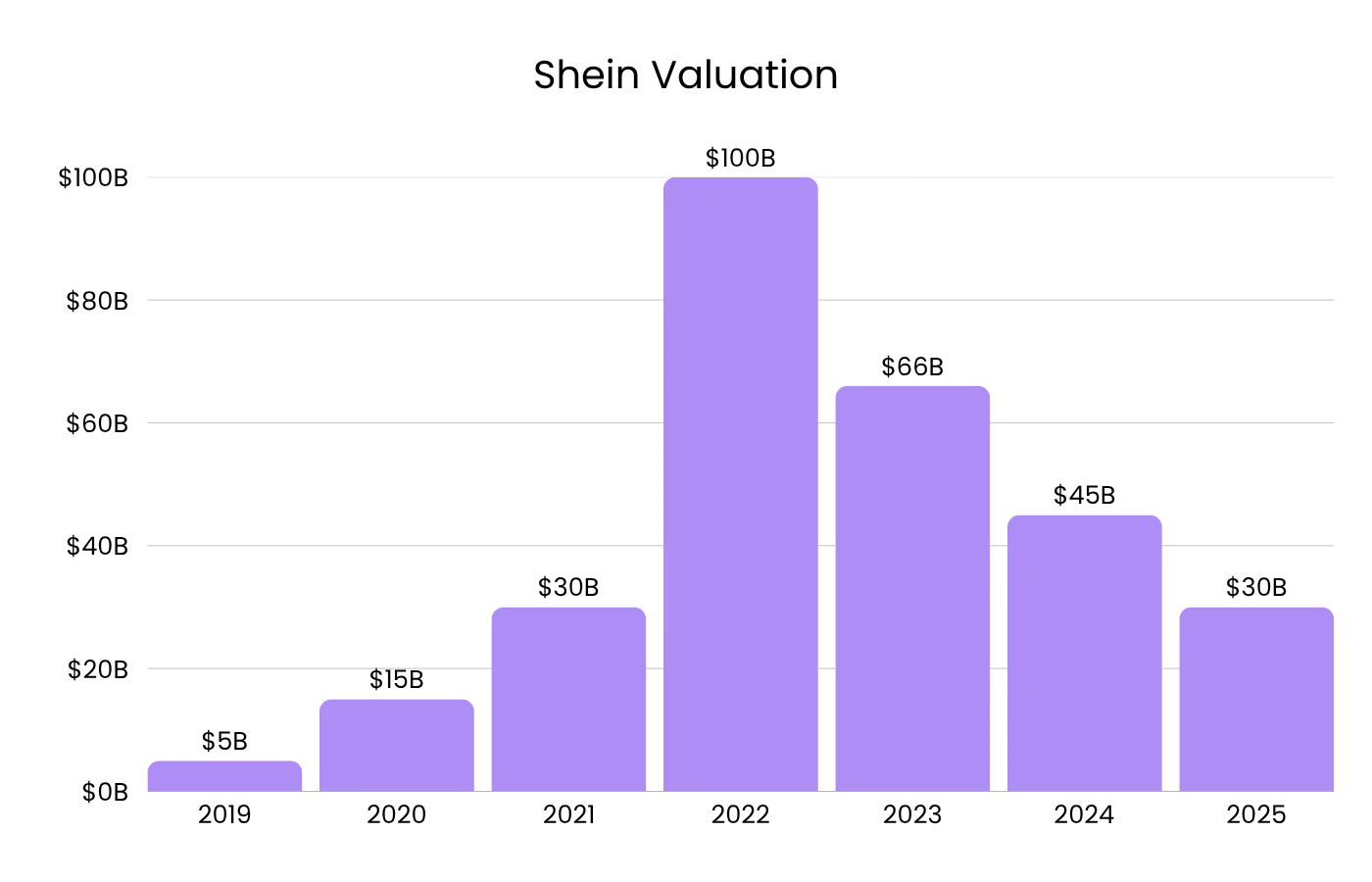

Temu Net Worth

As Temu is a privately held company, there’s no data available to the public about the company’s net worth.

We do know that PDD Holdings, Temu’s parent company, has a net worth of $128.79 billion. As Temu makes up a minority of the assets owned by PDD Holdings, we can assume that Temu’s net worth is less than that of Shein ($100 billion), and far behind Amazon, which is worth nearly $1.5 trillion.

Temu App Statistics

As of July 2023, the Temu app had over 130 million downloads in the space of less than a year.

As of the end of 2022, this was sitting at 15 million. The app was reportedly downloaded over 30 million times in the month of July.

With these numbers, Temu sits as the #1 shopping app in the US in both the Google Play Store and Apple App Store.

Most of Temu’s downloads come in the US, with a little over 42% of their total app downloads. Temu’s next most popular countries are the UK, France, Germany, Italy and Spain.

According to Similarweb, the Temu app’s usage rate ranks #3 in the US for the “Shopping” category, and 43rd among all apps.

Temu Traffic Statistics

Similarweb estimates Temu.com receives 286.6 million visits per month.

The site is ranked as the #6 marketplace website in the US, behind Amazon, eBay, Walmart, Etsy and Target.

Overall, Temu.com ranks as the 72nd biggest website by traffic in the US, and 92nd globally.

If you’re running an eCommerce store, and you don’t have an app, you’re missing out. Our eCommerce App Revenue Calculator shows just how much you can gain from launching your own app.

How Did Temu Get So Big?

Temu’s ability to source products directly from Chinese manufacturers is a big reason for the platform’s growth, enabling them to sell products at huge discounts and undercut the competition.

Even though the quality of the products sold on Temu is often questionable, these low prices make consumers willing to take the risk.

Temu also relies on quite aggressive marketing strategies, such as >90% discounts, gamification tactics, app-exclusive discounts and very persistent notifications.

There are reports of Temu getting in touch with users over 100 times within the space of three weeks, through a variety of channels including push notifications, email and SMS.

Temu also invests heavily in social media marketing, specifically using influencers to gain visibility on TikTok with younger customers. They also ran multiple advertisements during the 2023 Super Bowl, which was many US consumers’ first introduction to the Temu brand.

Does Temu Make a Profit?

It’s believed that Temu does not make a profit at this time. An article on WIRED suggests that the company loses an average of $30 per order, for overall losses of $588 million to $954 million per year.

This is partly due to the low margins required to sell products at steep discounts, along with their aggressive marketing as the company tries to gain market share in the US, reportedly carrying a marketing budget of $1 billion per month.

Learn more: see how Temu uses push notifications to drive repeat sales and build a habit of daily use, in this article.

Will Temu Continue to Emerge as One of the World’s Biggest Shopping Apps?

Temu carries significantly more controversy with its rise than Shein, another big new player in the eCommerce market.

Most of what you read about Temu online is negative, from questions about the legitimacy of products for sale on the site, to worker exploitation and data privacy concerns.

Their user acquisition and marketing strategy is also extremely aggressive, to the point where some may say it’s exploitative.

Yet despite all this, Temu’s user base continues to grow, and it continues to hold the top spot for downloads in Google Play and the App Store.

As it currently stands, Temu is unprofitable, and thus their current operating model is unsustainable. Their road to profitability is to build the Temu brand as a household name in the US market, along with bringing in more marketplace sellers to adopt a model similar to Amazon’s.

However, as long as Temu relies on low-cost, low-quality goods from China, it will always carry a stigma that will prevent it from challenging Amazon as the marketplace eCommerce leader.

Sources

Statista | Business of Apps | Tech Buzz China | Macrotrends | AppFigures | Similarweb | WIRED

.avif)

.avif)